Failure Case Study: Why Tally (Fintech App) Shut Down in 2024?

It started with a confusing email and a sudden app notification. For thousands of Americans relying on Tally to manage their credit card debt, the news in August 2024 wasn’t just surprising—it was panic-inducing. After nine years of promising to automate debt freedom, Tally shut down, leaving users wondering what would happen to their lines of credit and sensitive financial data.

If you are reading this, you might be a former user scrambling to understand why your “financial automated assistant” disappeared overnight, or you might be a fintech enthusiast analyzing the fintech funding crunch of 2024.

In this deep-dive case study, we will uncover the real reasons behind Tally’s collapse, explain exactly what the transfer to Systems & Services Technologies (SST) means for your wallet, and provide actionable steps to protect your credit score.

The Rise and Sudden Fall of Tally

What Was Tally’s Promise?

Founded in 2015, Tally pitched a seductive value proposition: it would act as a robo-advisor for your credit card debt. The app offered a low-interest line of credit to pay off high-interest cards, automating the payments so users never missed a due date.

For a long time, it worked. Tally raised over $170 million from top-tier venture capitalists like Andreessen Horowitz. But in 2024, the math stopped adding up.

Reason 1: The Fintech Funding Crunch

The primary driver for the Tally app shut down was a severe lack of capital. In the “zero-interest rate policy” (ZIRP) era, startups could easily raise money to burn on customer acquisition. However, as the Federal Reserve raised interest rates to combat inflation, venture capital dried up.

Expert Insight: “In my experience analyzing fintech market cycles, models that rely heavily on constant external funding rather than early profitability are the first to crumble when interest rates rise. Tally’s burn rate likely outpaced its ability to monetize its user base effectively.”

Reason 2: The Failed Pivot to B2B

Realizing the consumer-direct model was bleeding cash, Tally attempted a “Hail Mary” pivot in April 2024. They sunsetted their consumer app to focus on a B2B (Business-to-Business) model, hoping to sell their technology to banks. Unfortunately, this pivot came too late. They couldn’t secure the necessary partners or funding to sustain operations during the transition.

The Aftermath: Transfer to SST (Systems & Services Technologies)

If you were a Tally user, you likely received a notice that your account was being transferred to a company called SST. This has caused significant confusion.

Who is SST?

Systems & Services Technologies (SST) is a third-party debt servicer. They are not a “debt buyer” in the traditional sense of a collections agency buying charged-off bad debt; rather, they are the new administrative servicer for the loan you originally took from Tally.

The “Payment Blackout” Chaos

During the transition in late August and early September 2024, there was a “payment blackout period” where users couldn’t make payments to Tally or SST.

-

The Risk: Many users feared late fees or missed payments during this window.

-

The Reality: While SST is legitimate, their user interface and customer service are not as modern or user-friendly as Tally’s tech-forward app.

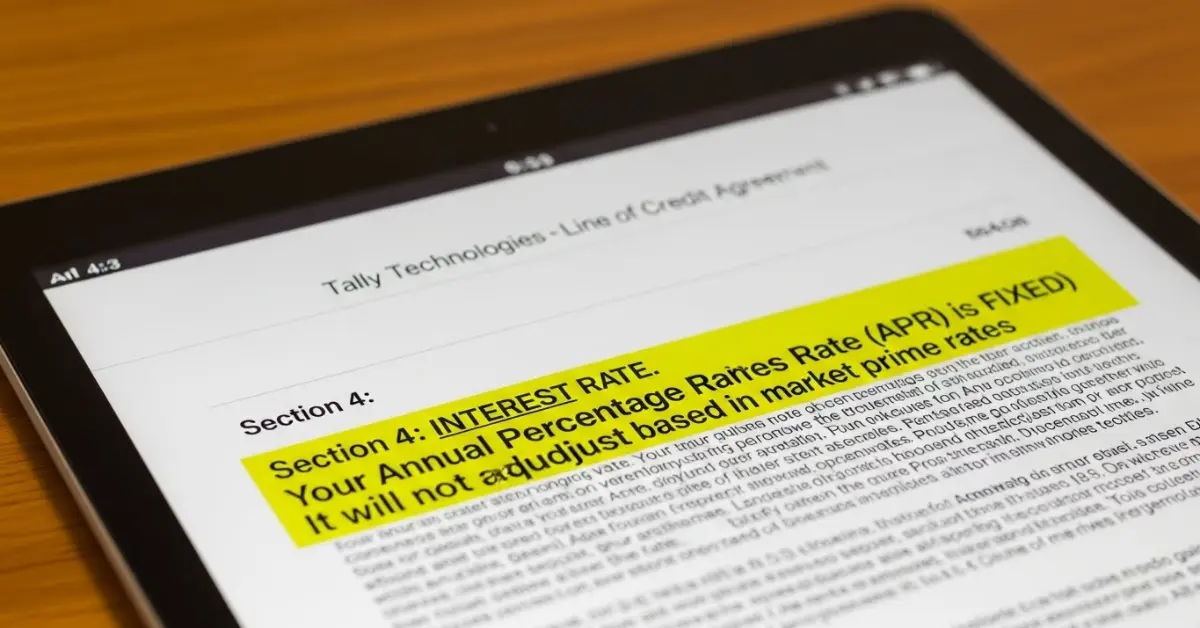

Will My Interest Rate Change?

Technically, the terms of your original loan agreement should stand. However, many users on forums like Reddit have reported confusion regarding their APR.

-

Action Item: You must locate your original Tally contract (PDF) immediately to prove your fixed APR if SST attempts to adjust it.

Immediate Steps for Former Tally Users

If you still owe money on your Tally line of credit, do not ignore the debt. Doing so will tank your credit score. Follow these steps immediately:

1. Set Up Your Account with SST

Go to the SST website and register using the new account number provided in your welcome letter. If you haven’t received a letter, call their support line immediately.

-

Tip: Verify that your balance matches what you saw in the Tally app before it went dark.

2. Switch to Manual Payments

Tally’s main selling point was automation. That is gone.

-

Warning: Do not assume Autopay carried over perfectly. Log in to SST and manually schedule your first payment to ensure no “missed payment” flags hit your credit report.

3. Check Your Credit Report

In roughly 30-45 days, the Tally trade line on your credit report will mark as “Closed” or “Transferred,” and a new line for SST may appear.

-

Monitor your credit utilization ratio. Since the Tally line is closed to new spending, your total available credit might drop, which can temporarily lower your score.

How a Small Coffee Shop Increased Sales by 40% Using TikTok | Full Case Study

Top Alternatives to Tally in 2024

Now that Tally is gone, you still need a strategy to manage debt. Here are the best debt consolidation app alternatives:

| App Name | Best For | Key Feature |

| Upstart | Personal Loans | Uses AI to approve loans for those with “fair” credit. |

| Happy Money | Credit Card Debt | specifically designed to pay off credit cards (The “Payoff Loan”). |

| SoFi | Good Credit Scores | Offers low rates and unemployment protection. |

| Avalanche Method | DIY Debt Payoff | No app needed; pay highest interest cards first manually. |

Author’s Note: I always advise caution with personal loans. Only take one out if the APR is significantly lower than your credit card APR. Otherwise, you are just moving debt around, not solving the problem.

Lessons for the Fintech Industry

The Tally fintech failure serves as a stark warning for the industry.

1. Unit Economics Matter More Than Growth

Tally spent heavily to acquire customers, betting that their “Lifetime Value” (LTV) would eventually pay off. In 2024, investors demanded immediate profitability, not theoretical future profits.

2. The Danger of “Feature vs. Product”

Critics often argued that Tally was a feature (automated payments) masquerading as a company. Banks and credit card issuers eventually caught up, offering their own automation tools, rendering Tally less unique.

3. Trust is Fragile

By shutting down the app abruptly and transferring users to a legacy servicer like SST, the brand equity of Tally evaporated instantly. Future fintechs must have better “wind-down” plans to protect user trust.

Conclusion

The shutdown of Tally in 2024 marks the end of a prominent era in consumer fintech. It was a victim of high interest rates, a difficult funding environment, and a business model that couldn’t adapt fast enough.

For former users, the priority now is administrative defense: validate your debt with SST, set up manual payments, and keep a hawk-eye on your credit report. The app may be dead, but your financial health is still very much alive—and entirely in your control.

What has your experience been with the transfer to SST? Let us know in the comments below—your insights could help others navigating this confusion.

Frequently Asked Questions (FAQ)

1. Is SST a legitimate company or a scam?

SST (Systems & Services Technologies) is a legitimate third-party loan servicer. They are not a scam, but they are a traditional debt servicer, meaning they lack the modern app interface Tally users are used to.

2. Will the Tally shutdown hurt my credit score?

It might. Because the Tally line of credit is effectively “closed” for new borrowing, your total available credit limit may decrease. This increases your credit utilization ratio, which can temporarily drop your score.

3. Can I stop paying my Tally debt?

No. Your debt remains valid; it has simply been transferred to a new servicer. If you stop paying, SST will report missed payments to credit bureaus, and they may send your account to a collections agency.

4. How do I access my old Tally records?

Since the app is offline, you cannot access old statements via the app. You must contact Tally’s support email (if still active for archives) or request a “debt validation” letter from SST, which should include the history of the debt.

5. What is the best Tally alternative for bad credit?

If you cannot qualify for a consolidation loan like SoFi or LightStream, consider credit counseling (via NFCC.org). They can often negotiate lower interest rates with credit card issuers without requiring a new loan.